The AnewZ Opinion section provides a platform for independent voices to share expert perspectives on global and regional issues. The views expressed are solely those of the authors and do not represent the official position of AnewZ

The International Monetary Fund (IMF) and World Bank held their Spring Meetings in Washington from 13 to 18 April. Finance ministers flew in, communiqués were drafted, and the usual parade of panels and press conferences ran their course.

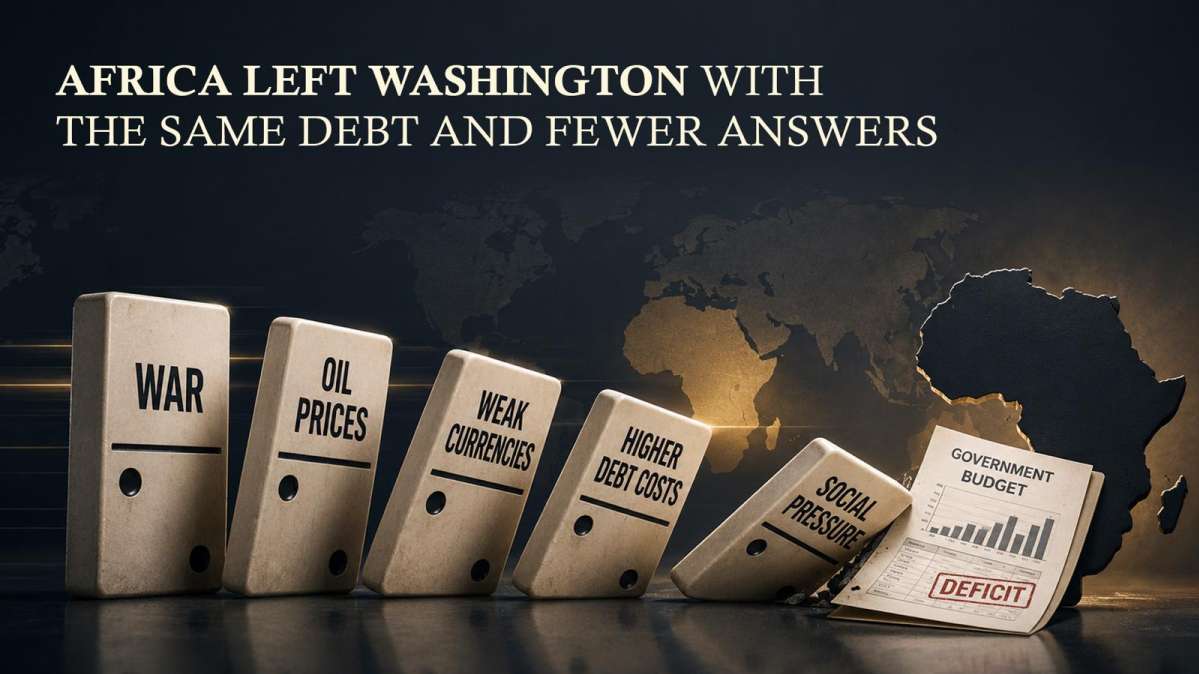

For Africa, the timing could not have been more urgent. Oil prices had already surged more than 50% since late February. Twenty-nine of the continent's roughly 42 currencies had weakened. Debt service obligations were consuming more than 31% of government revenues across the continent, and a war in the Middle East that African governments had no hand in starting was making all of those numbers worse by the week.

Africa left Washington without a serious debt restructuring framework. Again.

Numbers that went into the Room

Before examining what came out of those meetings, it helps to understand the weight of what went in.

African governments collectively carry nearly $2 trillion in public debt. According to data presented at the Spring Meetings, in 2025 African governments spent nearly a fifth of their revenues on interest payments alone. Four out of every five African countries spent more on debt service than on health or education. Seven countries are already in debt distress and another thirteen are considered at high risk.

Those were the baseline figures before the Iran conflict added a new layer of pressure on currencies, import costs and fiscal balances.

The IMF's own projections, released alongside the meetings, revised Africa's growth outlook downward from 4.5% in 2025 to 4.2% in 2026.

The African Consultative Group, which brings together African finance ministers and central bank governors to meet with IMF management during the Spring Meetings, issued a joint statement with IMF Managing Director, Kristalina Georgieva, acknowledging that the war was adding fresh complexity to an already strained outlook, with the potential for what the statement carefully called "severe scarring." That is diplomatic language for a slow-moving crisis that is very difficult to reverse once it takes hold.

What the meetings actually delivered

The IMF Managing Director indicated that near-term demand for IMF financing could reach $50 billion. World Bank President, Ajay Banga, spoke of $20 to $25 billion in rapid financing. Both institutions deserve credit for stepping up with numbers that at least acknowledge the scale of the emergency.

But as the Center for Global Development noted during the meetings, the envelope of concessional financing available to the continent's poorest economies remains tightly constrained. The commitments made were incremental, shaped by the fiscal caution of donor governments and the increasingly fractured politics of multilateral institutions. There were no significant breakthroughs on debt relief.

The G20's Common Framework for debt restructuring, which was supposed to streamline the process for countries in distress, once again came in for criticism over its persistent delays and its failure to bring private creditors fully into the process.

Ghana's experience is instructive here. Zambia's too. Both countries navigated painful restructuring processes and both are held up as success cases. But Ghana spent years in a debt crisis before reaching restructuring agreements, and its economy is only now stabilising.

The lesson the continent keeps drawing from these cases is that the system works, eventually, for countries prepared to absorb years of economic pain in the meantime. For governments now facing a simultaneous energy shock, currency depreciation and rising food costs, "eventually" is not a viable answer.

War changed the calculus

What made this year's Spring Meetings different from previous editions was the Iran conflict sitting squarely in the middle of every conversation about African debt sustainability.

Currency depreciation is not simply a financial inconvenience. When a currency weakens, the cost of servicing dollar-denominated debt rises in local currency terms even if the interest rate stays the same. For a government already spending 31 cents of every revenue dollar on debt, a 10% depreciation in the local currency means that debt burden effectively grows without a single new loan being taken out.

Egypt's pound lost nearly 11% of its value against the dollar between 1 March and early April. The Ugandan shilling, the Ghanaian cedi and currencies across the continent followed similar trajectories.

BMI, the research unit of Fitch Solutions, warned during the conflict that Burundi's franc and Malawi's kwacha face particular devaluation risk as high energy import costs erode what little foreign exchange buffer those countries have left.

Burundi and Malawi are the kinds of economies where a sustained energy shock does not stay in the realm of fiscal statistics for long. When foreign exchange buffers run dry and fuel becomes scarce, hospitals start rationing, supply chains seize up and the distance between a difficult year and a genuine humanitarian emergency shrinks very quickly.

Conversation Africa actually needs

At the Spring Meetings, African policymakers pushed for time-bound restructuring processes under the Common Framework and stronger enforcement of comparable treatment between private and official creditors. The Bank of Ghana governor called directly for fixing the sovereign debt resolution system, describing the current pace as inadequate given the scale and persistence of overlapping shocks. Those calls were noted. Whether they translate into reform is a different matter entirely.

What the continent needs is a debt architecture that can move at the speed of a crisis rather than the speed of a negotiation. The IMF and World Bank have the analytical tools and the institutional weight to push for that. What has been missing, Spring Meetings after Spring Meetings, is the political will among the major economies to actually build it.

A war nobody in Africa voted for has now made the cost of that inaction visible to everyone. The question is whether Washington was listening.

What is your opinion on this topic?

Leave the first comment